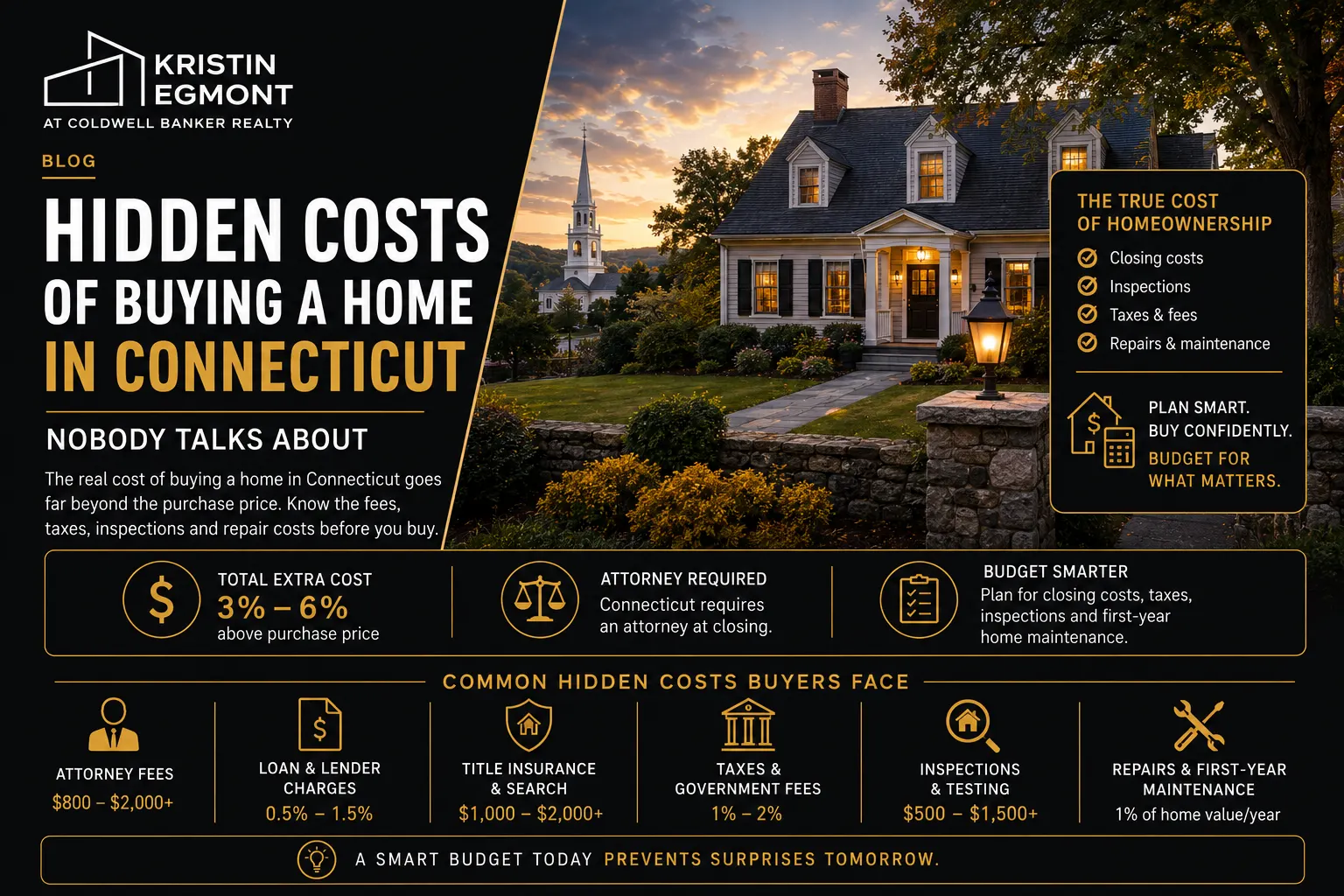

Everyone knows buying a house costs a lot, but the extra costs besides the home’s price might catch you off guard.

For homebuyers, the added expenses of mortgage requirements, closing costs, and other fees can pile up. Kristin Egmont can guide you through these hidden costs for realtors in Connecticut and beyond, helping you to understand and potentially reduce them. By getting familiar with these extra charges, you’ll be better prepared for your home purchase, avoiding surprises and possibly even skipping some of the unnecessary costs.

Read on to learn about these hidden costs so you can budget smarter and keep from spending too much when buying and owning a home.

What are the Hidden Costs of Buying a House?

The hidden costs of buying a house refer to the unexpected or lesser-known financial expenses associated with purchasing and owning a home. These costs go beyond the purchase price and can include fees for legal services, taxes, insurance, maintenance, and other expenses that may not be immediately apparent.

Understanding these costs is crucial for budgeting accurately, making informed investment decisions, and avoiding financial strain.

Why do Hidden Costs Matter?

- Budget Planning: Understanding hidden costs is essential for accurate budget planning. Knowing these costs upfront helps avoid surprises that could disrupt your financial planning.

- Real Cost of Homeownership: Hidden costs reveal the true cost of owning a home. What seems like a good deal at first may not be so once all the additional expenses are taken into account.

- Financial Preparedness: Being aware of hidden costs prepares you financially for the road ahead. This means you can save or arrange the necessary funds to cover these expenses.

- Investment Decision: Knowledge of hidden costs aids in making an informed investment decision. It helps you assess whether a property is worth its price when considering all associated expenses.

- Negotiation Leverage: Understanding all possible costs can give you leverage in negotiations. You might negotiate a better purchase price or terms once you’re aware of all the expenses involved.

- Avoiding Financial Strain: Hidden costs can add up quickly, potentially putting you in a tight financial spot. Knowing these costs ahead of time helps avoid undue stress and financial strain.

- Long-term satisfaction: Being prepared for all expenses ensures there are no regrets or feelings of being misled later on. This preparation leads to long-term satisfaction with your home purchase.

- Planning for upkeep and maintenance: Some hidden costs are related to the future upkeep and maintenance of the property. Being aware of these helps in planning for the long-term care and value retention of your home.

6 Most Important Hidden Costs

Here are some of the hidden costs that you should be more aware of.

-

Stamp Duty and Registration Fee

When purchasing a property, one must register it with the government and pay the corresponding stamp duty fees.

By understanding the nuances of stamp duty and registration fees and taking proactive steps, buyers can effectively plan their budget and avoid financial surprises during the property transaction. Let’s delve into how being informed about these fees can help reduce overall costs:- Stamp Duty: Governments impose taxes on legal documents, usually those involving the transfer of a real estate or other assets, called stamp duties. Stamp duties, also called stamp taxes, are levied by governments on documents required to lawfully document certain kinds of transactions. These documents include marriage licenses, military commissions, patents, copyrights, and other legal records.

- Budgeting Considerations:

- It is crucial for accurate budgeting during the home-buying process.

- Regional rates vary; thorough research into specific regulations is necessary.

- Awareness of potential exemptions or reductions is important.

- Property Trends:

- Our experts help you calculate stamp duty based on the property’s current or expected value.

- They regularly review your budget and make necessary adjustments to accommodate any changes in stamp duty due to fluctuations in property value.

-

Closing and Mortgage Expenses

- Mortgage Broker Fee: Hiring a mortgage broker can be a crucial first step in becoming a homeowner. This expert simplifies the process of finding a good mortgage by serving as your point of contact with possible lenders. But there is a price for the convenience: a broker’s fee. Even though it might not seem like much in the big picture, it is a cost that can add up and might catch you off guard if you are not prepared.

- Fees for Underwriting and Processing: Obtaining a mortgage involves a lot of paperwork, most of which is handled by underwriting and processing. These costs are essential for the administrative processing required to grant your loan. They carry a financial burden that requires prior awareness and planning, even though they might appear to be just another step in the process.

- Appraisal Fee: The property appraisal is a necessary step before completing your mortgage. This procedure determines the home’s value and makes sure it matches the loan amount. Although the appraisal fee is often overlooked when considering the total cost of a house purchase, it is essential and can come as a surprise if not planned for.

- Credit Report Fee: Before approving a mortgage, a thorough review of your credit history is required. The credit report fee is the price for this investigation. Despite the fee’s seeming standardness, it adds another level of financial planning to the home-buying process.

- Discount points on interest rates: Buying discount points lowers your mortgage interest rate by requiring an upfront payment at closing. This can be a big expense that might surprise you if you do not account for it in your initial budgetary calculations.

- Escrow Fees: The last phase of the home-buying process is the transfer of ownership, which is a task that is associated with escrow fees. The administrative tasks required to complete the sale are covered by these fees. Despite being crucial, they are frequently disregarded and may come as a surprise if not planned for in your budget.

-

Maintenance Fee Deposit

It’s important to think about maintenance fees, as these fees add to the total cost of owning your home.

- Understanding Homeownership Costs: Owning a home isn’t just about paying for the house itself. There are extra costs too, like maintenance fees. These are important because they add to what you spend on your home.

- Initial Costs for New Homes: When you get a new home, the people who built it usually ask for some money ahead of time. This is for caring for shared spaces like parks and streetlights, to keep them looking good and working well for the first 1-2 years.

- Deposits for Existing Properties: Moving into a building that’s already there? You’ll likely need to pay a deposit too. This helps cover the cost of fixing things in the future and keeps the building in good shape. How much you pay depends on how many shared facilities there are and how the building handles these fees.

- Amenities and Maintenance Fees: If your building has lots of extra features like a swimming pool or a gym, you might pay more. It’s good to look at what you’re getting and decide if it’s worth the extra cost for you.

- Deciphering Maintenance Fees: Get to know the maintenance fees where you’re moving. If the place is well taken care of, you might not need to pay as much. Talk to the managers to understand the costs better.

-

Brokerage Service Cost

- Budgeting for Brokerage Fees: When planning your budget for a new house, don’t forget about brokerage fees. These are easy to overlook but can surprise you later on because they’re apart from the big costs, like the down payment.

- Understanding Fee Variability: The fee for using a broker can be between 1-2% of the house’s price, but it might be more for complicated deals or more expensive homes. Knowing this helps you plan better.

- Discussing Fees Upfront: Have a chat about all the brokerage fee details at the start. This includes what the fee covers and any extra costs. It helps avoid confusion later.

- Evaluating Broker Services: Find out what the broker does for their fee. Some offer more services than others. Knowing what you’re paying for helps you choose the right broker.

- Negotiating Brokerage Costs: Sometimes, you can talk about the fee and possibly get a better deal, especially if your purchase is unique. It’s about finding a balance that works for both you and the broker.

-

Parking Space Charges

- Parking Cost Consideration: When buying a house, remember that getting a parking space costs extra. It’s not included in the house’s price, and thinking about this cost helps you understand the total amount you’ll spend.

- Parking Separate Expense: Parking costs extra on top of the house price. Whether a space is included or not is crucial to figuring out your overall costs.

- Parking Price Evaluation: The cost of a parking space can vary a lot based on where it’s located and how big it is. It’s worth taking a close look to decide if it’s worth the price for you.

- Budgeting for Parking: Include the cost of parking in your budget from the start. If you don’t, you might miss out on getting a space, which could be sold to someone else.

Parking Negotiation Rules You can negotiate the price or terms for the parking space. Also, every community has its own rules about parking. Knowing these can help you avoid surprises later.

-

Interior Decoration Cost

When you buy a house, you might not realize how much you need to spend to make it feel like home. This part of your budget covers everything to make your living space comfortable and styled just for you.

- Necessary and Unavoidable: Making a house your home means more than just moving in. It involves spending on things you might not see at first but feel essential later, like painting walls, fixing plumbing, choosing furniture, and buying appliances. These steps are crucial for comfortable living and personalizing your space.

- Diverse Range of Expenses: The costs of setting up your home can vary widely. For instance, you can choose between basic painting and more elaborate designs; plumbing might require simple repairs or major upgrades; and your choices in furniture and appliances can range from budget-friendly to luxury items. Each decision reflects your taste and how much you’re willing to invest in your home.

- Financial Commitment: Dressing up your home to match your vision can cost up to $ 10,000 to $ 13,000, showcasing the hidden expenses of making a space truly yours. Planning a specific budget for interiors is wise, helping you manage these hidden costs without overspending. This way, you uncover and address these unseen expenses, ensuring your dream home doesn’t become a source of financial stress.

Other Hidden Costs you must watch out for Before Buying a House

Here are some of the additional hidden costs that you must be aware of:

- Title Search Fee: This fee ensures there are no legal issues with the property’s ownership. It’s a vital step in the home-buying process that can be costly if you’re not prepared for it.

- Title Insurance: Title insurance protects you against any legal issues that might arise with the property’s title. While it’s essential for your peace of mind, it’s an extra cost that can catch you by surprise.

- Property Taxes: Property taxes can be a significant expense that you need to budget for. If you’re not prepared to cover these costs, they can become a hidden burden.

- Transfer Tax: When ownership of the property changes hands, there’s a tax involved. It’s an additional expense that can catch you off guard if you’re not aware of it.

- HOA Dues: In a neighborhood or condominium association, homeowners association (HOA) dues are the fees a homeowner pays for maintenance, improvements, and repairs. If you’re buying a property in a community with a homeowners association, you’ll need to pay monthly dues. These ongoing expenses can add up over time and become a hidden cost of homeownership.

- Moving Costs: Moving can be expensive, especially if you’re hiring movers or renting a truck. It’s an additional expense that you need to budget for when buying a home.

Utilities: Once you move into your new home, you’ll need to pay for utilities like electricity, gas, and water. These ongoing expenses can become a hidden cost if you’re not prepared for them.

How to Prepare Ongoing and Future Expenses?

This is one of the most important parts of what you read until now. So, without further ado, let’s get started:

- The Underestimated HVAC (Heating, Ventilation, and Air Conditioning) Factor: Homeownership often brings unforeseen costs, notably in maintaining the heating, ventilation, and air conditioning (HVAC) system. This essential aspect of a comfortable home environment can lead to unexpected expenses, underscoring the importance of incorporating it into your financial planning.

- The Roof Over Your Head: The stability and safety provided by a home’s roof come with their share of silent expenses. Preparing for the inevitable wear and tear on this crucial part of your house is vital, as neglecting it could lead to substantial financial strain.

- The Plumbing Predicament: The complicated nature of a home’s plumbing system can often lead to sudden and unforeseen expenses. Regular maintenance is a preemptive step homeowners must consider to avoid being caught off guard by costly repairs.

- The Emergency Fund Imperative: An often overlooked aspect of financial planning for homeowners is the establishment of an emergency fund. This fund acts as a financial buffer, safeguarding against the unpredictability of home-related expenses and ensuring peace of mind in the face of unforeseen costs.

End Note!

Understanding and managing the hidden costs of buying a house can make the journey to homeownership less stressful and more rewarding. With proper guidance, you can navigate these expenses, plan effectively, and even find ways to lower them.

Remember, while the costs of buying a home can be high, being prepared and informed helps you tackle them head-on. Consider investing in a home warranty as a smart way to protect against unexpected repair costs, making your new home a source of joy rather than anxiety. This way, you’re not just buying a house; you’re wisely investing in your future comfort and security.

Additionally, many people need to sell their current home before they can afford to buy a new one because their money is tied up in their old house. This makes it hard for them to make a down payment on a new house without selling their old one first.

The “buy before you sell” option lets you purchase your dream home while giving you time to sell your old one, so you don’t have to worry about paying two mortgages at once. Kristin Egmont can assist you with finding houses for sale in Easton, CT, and Fairfield, CT, among others, making the transition smoother and more manageable.

")